AI is clearly mainstream. The skyrocketing user growth on the big AI platforms, the threat to Web 2.0 household names like Google and Meta, the roller coaster of the AI chip makers: AI has filled headlines for a few years now.

AI platforms are on a well-traveled monetization journey. In the first wave, they've managed to grow direct monetization. Millions of users have translated into a certain percentage of Pro, Plus, Business, or — insert premium version name of choice. New users are probably growing at a predictable rate. Conversion rates for paying customers are stubbornly low. With the first wave of direct monetization in motion, they are following the lead of their tech giant ancestors and are making hard pushes into commerce.

ChatGPT Shopping | Source: OpenAI

I'll borrow from my own recent experience to illustrate what agentic commerce is. In a brief moment of weakness and stupidity, my wife and I agreed to co-host a first-grade PTA fundraiser. I mostly forgot about it until my wife reminded me a few days ago that we had 120 guests RSVPed. We now had to order pizza and beverages for 60 adults and 60 kids. Now, my smart wife went straight to ChatGPT to figure out how many pizzas, wine, beer, and what else we needed. Predictably, AI gave us a very precise and accurate answer. Who knew it would take 20 Mountain Mike's pizzas (double-sliced) to feed this group? Magically, AI had taken us right to the water's edge of decision-making. However, it couldn't close the deal.

Problem #1 - Is it a BOT or an AI Agent?

When I used to work at a global payment network, I couldn't help but smirk when I heard the term “friendly fraud.” I think it was the slight oxymoron that made me laugh. But there it was, meeting after meeting. “Friendly fraud” was always talked about as a somewhat unavoidable part of payments. The occasional chargeback or refund was inevitable from an otherwise upstanding cardholder. “Friendly fraud” was often mentioned in the same breath as its far more sinister cousin “programmatic fraud.” This is where my smirk usually stopped. Folks leaned in and got serious.

Networks, processors, and fraud prevention services have spent decades trying to stop “programmatic fraud”. In digital commerce, “programmatic fraud” almost always materializes at the merchant's front door as a BOT. A BOT is a computer program that performs automatic repetitive tasks. And much of the modern payment infrastructure is built to stop BOTs.

As a simple starting point, agentic commerce needs to solve the problem of convincing the rest of the payments infrastructure that it is an agent and not a BOT.

Problem #2 - Agentic Commerce Transaction Anatomy: Agents, Merchants, Networks, Processors all need payment info

Ecosystem reality check....

Storing PCI (card) data is cumbersome. Merchants avoid it.

Merchants want and value payment information. For example, recurring payments, one-click checkouts, and refund management all require payment information.

To access payment information without storing payment information, many merchants depend on tokens.

Payment tokens are almost always a bilateral relationship between the vault which is also the token creator (e.g. Network, Processor, VGS) and the token requestor (e.g. merchant).

So the transaction starts with the AI agent. The Pro, Plus, Business, or — insert premium version name of choice user pays for their subscription. The payment information will likely be converted to be used for agentic commerce transactions for future purchases. Most of the AI platforms were founded in the last five years - they grew up not holding card data and depend on tokens. Their tokens probably come from their PSP (e.g. Stripe, Adyen, Braintree). These PSPs are modern and quite capable. In my above example, if the pizza place (e.g. Mountain Mike's Pizza) and the drink place (e.g. Costco) use the same PSP as the originating AI agent, the PSP can probably handle the end-to-end agentic AI transaction.

What if the PSP for the Merchant and the originating AI company is different? What happens?

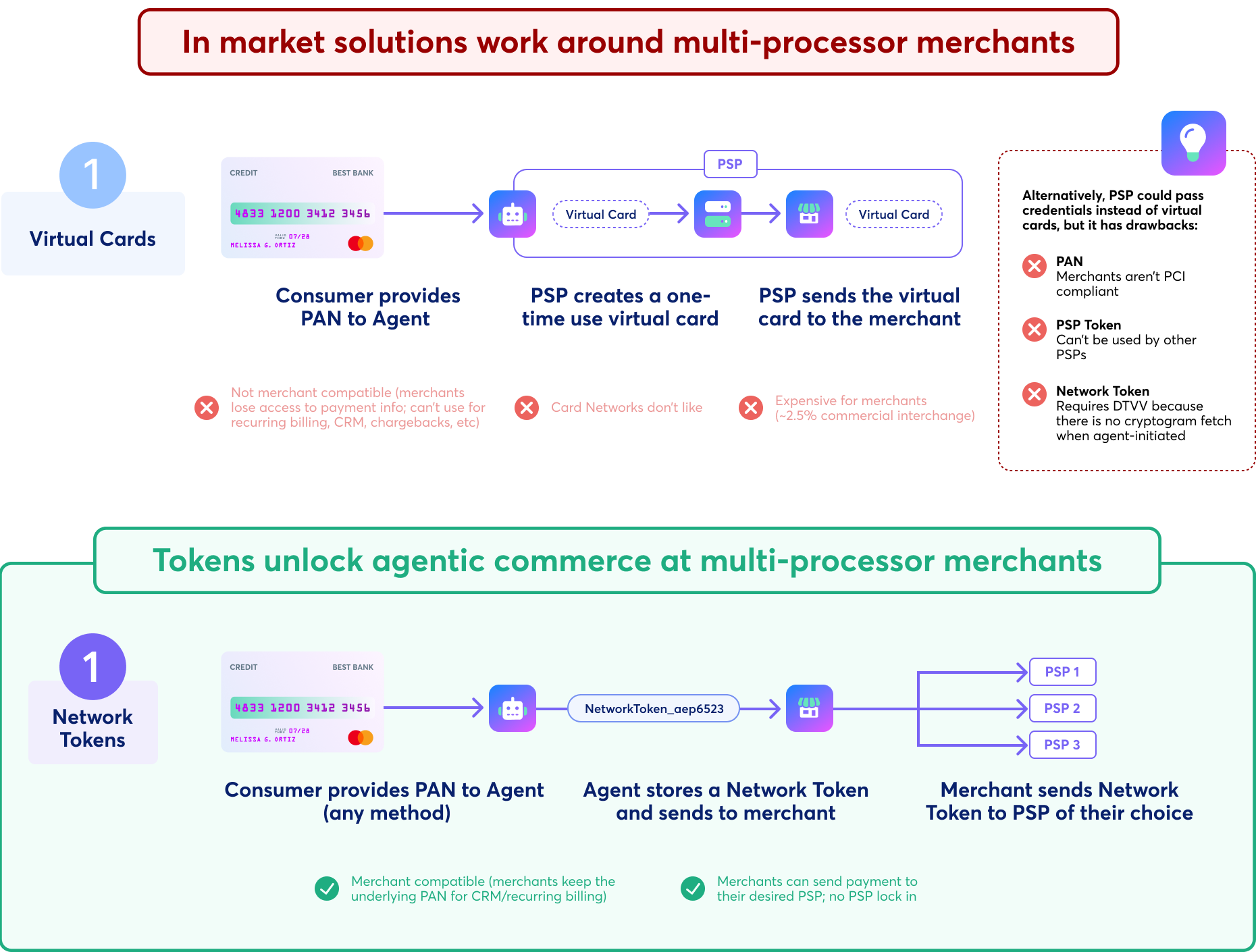

Solution 1: Virtual Cards

Today, one common way we see this being solved in the market is through the use of virtual cards. This is where an agent (via their PSP) creates one-time, single-use virtual cards that are sent to the underlying merchant of record (MOR). This is problematic for three reasons: 1) merchants lose access to the payment information, which they often use for anything from recurring billing to fraud to their CRM, 2) the card networks and merchants dislike this because it typically increases the cost of acceptance, and 3) it creates customer confusion and a nightmare for chargebacks (the card the consumer used to pay isn't the card shown on the receipt). So while this has been a good way to get something to the market quickly, it's unlikely it will be a good long-term solution.

Solution 2: Network Tokens

Now let's circle back to tokens as a potential solution. Network tokens have become more commonplace and widely used (Mastercard has notably stated that they are getting rid of PANs in place of network tokens by 2030). These tokens are network-issued and obfuscate the underlying PAN but always ensure the card is updated because they are directly connected to the issuer via their network. Adoption of network tokens has been fantastic. Visa has seen 50% of all ecomm transactions take place on network tokens. Despite this proliferation, a gap exists.

There is a structural limitation today. Network tokens are generally being provisioned by PSPs on behalf of the merchant. Remember reality check #4. Most of the network tokens in the market today are specific to a PSP and Merchant combination. This means that the AI platform generated network token from PSP #1 can't be smoothly be transmitted to merchant PSP #2.

Network tokens seems like absolutely the right starting point. There is a gap in the market today to make network tokens smoothly flow across the ecosystem.

Takeaway

Tokens are the last mile of agentic commerce enablement. They unlock agentic commerce at multi-processor merchants.

Agentic commerce is going to require that AI platforms solve the last mile of payments and connect agents, merchants, networks, processors to unlock meaningful revenue beyond just subscriptions. The infrastructure is close, but not yet built, for agents that initiate and complete transactions across the fragmented merchant ecosystems. Tokens are the connective tissue that will allow AI agents to act on behalf of users at scale. Solving this last mile—securely, flexibly, and PSP-agnostically—will be required for the next era of digital commerce. And I would be remiss if I didn't close with one reminder: VGS tokens (both PCI tokens and network tokens) were built to be transmitted to third parties, solving the problem of uniting the multiple parties needed to enable agentic commerce at scale.

Learn More